Appendix: Ergodic Markov Chains and Stationary Distributions

Motivating Example: Long-Run Behaviour in a Cycling System ¶ Consider a simple weather model with two states: Sunny (S S S R R R

P = ( 0.7 0.3 0.6 0.4 ) P = \begin{pmatrix}

0.7 & 0.3 \\

0.6 & 0.4

\end{pmatrix} P = ( 0.7 0.6 0.3 0.4 ) Unlike the maze from Appendix A2 , this chain has

no absorbing state. The system cycles indefinitely between S S S R R R

This appendix develops the theory behind this observation: when does a Markov

chain converge to a unique long-run distribution, and how is that distribution

computed?

Theory ¶ Definition: Irreducible Markov Chain ¶ A Markov chain is irreducible if every state is reachable from every other

state. That is, for all states i i i j j j t ≥ 1 t \geq 1 t ≥ 1 ( P t ) i j > 0 (P^t)_{ij} > 0 ( P t ) ij > 0

Irreducibility means the chain cannot be split into disconnected parts that

never communicate. For example, a chain where state 1 can only reach states

1 and 2, while state 3 can only reach itself, is not irreducible.

Definition: Aperiodic Markov Chain ¶ A state i i i period d i = gcd { t ≥ 1 : ( P t ) i i > 0 } d_i = \gcd\{t \geq 1 : (P^t)_{ii} > 0\} d i = g cd{ t ≥ 1 : ( P t ) ii > 0 } aperiodic if d i = 1 d_i = 1 d i = 1 aperiodic if all

states are aperiodic.

Intuitively, an aperiodic chain does not get “trapped” in a cycle that forces

it to return to a state only at fixed multiples of some period d > 1 d > 1 d > 1

Definition: Ergodic Markov Chain ¶ A finite Markov chain is ergodic if it is both irreducible and

aperiodic .

Theorem: Ergodic Theorem for Finite Markov Chains ¶ If a finite Markov chain with transition matrix P P P

There exists a unique stationary distribution π ∈ R n \pi \in \mathbb{R}^n π ∈ R n

π P = π and ∑ i = 1 n π i = 1 , π i > 0 ∀ i . \pi P = \pi \qquad \text{and} \qquad \sum_{i=1}^n \pi_i = 1,\quad \pi_i > 0\ \forall i. π P = π and i = 1 ∑ n π i = 1 , π i > 0 ∀ i . For any initial distribution π ( 0 ) \pi^{(0)} π ( 0 )

lim t → ∞ π ( 0 ) P t = π . \lim_{t \to \infty} \pi^{(0)} P^t = \pi. t → ∞ lim π ( 0 ) P t = π . The long-run fraction of time spent in state i i i π i \pi_i π i

The stationary distribution π \pi π P P P

π ( P − I ) = 0 subject to ∑ i = 1 n π i = 1. \pi (P - I) = 0 \qquad \text{subject to} \qquad \sum_{i=1}^n \pi_i = 1. π ( P − I ) = 0 subject to i = 1 ∑ n π i = 1. Equivalently, since ( P − I ) (P - I) ( P − I )

Example: Stationary Distribution of a 2-State Chain ¶ Consider a Markov chain with two states { A , B } \{A, B\} { A , B }

P = ( 1 − α α β 1 − β ) P = \begin{pmatrix}

1 - \alpha & \alpha \\

\beta & 1 - \beta

\end{pmatrix} P = ( 1 − α β α 1 − β ) where 0 < α , β < 1 0 < \alpha, \beta < 1 0 < α , β < 1

The stationary distribution satisfies π P = π \pi P = \pi π P = π

π A ( 1 − α ) + π B β = π A ⇒ π A α = π B β \pi_A (1 - \alpha) + \pi_B \beta = \pi_A

\qquad \Rightarrow \qquad

\pi_A \alpha = \pi_B \beta π A ( 1 − α ) + π B β = π A ⇒ π A α = π B β Combined with π A + π B = 1 \pi_A + \pi_B = 1 π A + π B = 1

π A = β α + β , π B = α α + β . \pi_A = \frac{\beta}{\alpha + \beta}, \qquad \pi_B = \frac{\alpha}{\alpha + \beta}. π A = α + β β , π B = α + β α . For the weather example in

Motivating Example: Long-Run Behaviour in a Cycling System α = 0.3 \alpha = 0.3 α = 0.3 β = 0.6 \beta = 0.6 β = 0.6

π S = 0.6 0.9 ≈ 0.667 , π R = 0.3 0.9 ≈ 0.333. \pi_S = \frac{0.6}{0.9} \approx 0.667, \qquad \pi_R = \frac{0.3}{0.9} \approx 0.333. π S = 0.9 0.6 ≈ 0.667 , π R = 0.9 0.3 ≈ 0.333. This means that in the long run, approximately 2 out of every 3 days are sunny,

regardless of the weather on the first day.

Example: Verifying Ergodicity and Computing the Stationary Distribution ¶ Consider the 3 × 3 3 \times 3 3 × 3

P = ( 0 0.6 0.4 0.3 0 0.7 0.5 0.5 0 ) P = \begin{pmatrix}

0 & 0.6 & 0.4 \\

0.3 & 0 & 0.7 \\

0.5 & 0.5 & 0

\end{pmatrix} P = ⎝ ⎛ 0 0.3 0.5 0.6 0 0.5 0.4 0.7 0 ⎠ ⎞ Step 1: Check irreducibility. Inspect P P P P 2 P^2 P 2

P 2 = P ⋅ P = ( 0.38 0.20 0.42 0.35 0.53 0.12 0.15 0.30 0.55 ) P^2 = P \cdot P = \begin{pmatrix}

0.38 & 0.20 & 0.42 \\

0.35 & 0.53 & 0.12 \\

0.15 & 0.30 & 0.55

\end{pmatrix} P 2 = P ⋅ P = ⎝ ⎛ 0.38 0.35 0.15 0.20 0.53 0.30 0.42 0.12 0.55 ⎠ ⎞ All entries of P 2 P^2 P 2

Step 2: Check aperiodicity. Since P 2 P^2 P 2 d i = 1 d_i = 1 d i = 1 i i i

Step 3: Solve π P = π \pi P = \pi π P = π We solve:

( π 1 π 2 π 3 ) ( 0 0.6 0.4 0.3 0 0.7 0.5 0.5 0 ) = ( π 1 π 2 π 3 ) \begin{align*}

\begin{pmatrix} \pi_1 & \pi_2 & \pi_3 \end{pmatrix}

\begin{pmatrix}

0 & 0.6 & 0.4 \\

0.3 & 0 & 0.7 \\

0.5 & 0.5 & 0

\end{pmatrix} \\

&=

\begin{pmatrix} \pi_1 & \pi_2 & \pi_3 \end{pmatrix}

\end{align*} ( π 1 π 2 π 3 ) ⎝ ⎛ 0 0.3 0.5 0.6 0 0.5 0.4 0.7 0 ⎠ ⎞ = ( π 1 π 2 π 3 ) This gives:

0.3 π 2 + 0.5 π 3 = π 1 , 0.6 π 1 + 0.5 π 3 = π 2 , 0.4 π 1 + 0.7 π 2 = π 3 0.3\pi_2 + 0.5\pi_3 = \pi_1, \quad

0.6\pi_1 + 0.5\pi_3 = \pi_2, \quad

0.4\pi_1 + 0.7\pi_2 = \pi_3 0.3 π 2 + 0.5 π 3 = π 1 , 0.6 π 1 + 0.5 π 3 = π 2 , 0.4 π 1 + 0.7 π 2 = π 3 Replace the third equation with π 1 + π 2 + π 3 = 1 \pi_1 + \pi_2 + \pi_3 = 1 π 1 + π 2 + π 3 = 1

π = ( 65 227 , 80 227 , 82 227 ) ≈ ( 0.286 , 0.352 , 0.361 ) . \pi = \left(\frac{65}{227},\; \frac{80}{227},\; \frac{82}{227}\right)

\approx (0.286,\; 0.352,\; 0.361). π = ( 227 65 , 227 80 , 227 82 ) ≈ ( 0.286 , 0.352 , 0.361 ) . Exercises ¶ Classify each of the following Markov chains as irreducible, aperiodic, and/or

ergodic:

P = ( 0 1 1 0 ) P = \begin{pmatrix}0 & 1 \\ 1 & 0\end{pmatrix} P = ( 0 1 1 0 )

P = ( 0.5 0.5 0.3 0.7 ) P = \begin{pmatrix}0.5 & 0.5 \\ 0.3 & 0.7\end{pmatrix} P = ( 0.5 0.3 0.5 0.7 )

P = ( 1 0 0 0 0.5 0.5 0 0.5 0.5 ) P = \begin{pmatrix}1 & 0 & 0 \\ 0 & 0.5 & 0.5 \\ 0 & 0.5 & 0.5\end{pmatrix} P = ⎝ ⎛ 1 0 0 0 0.5 0.5 0 0.5 0.5 ⎠ ⎞

For each ergodic chain, compute the stationary distribution.

Let P = ( 1 − a a b 1 − b ) P = \begin{pmatrix}1-a & a \\ b & 1-b\end{pmatrix} P = ( 1 − a b a 1 − b ) 0 < a , b < 1 0 < a, b < 1 0 < a , b < 1

Show that this chain is always ergodic for any a , b ∈ ( 0 , 1 ) a, b \in (0, 1) a , b ∈ ( 0 , 1 )

Derive the stationary distribution ( π 1 , π 2 ) (\pi_1, \pi_2) ( π 1 , π 2 ) a a a b b b

Under what condition on a a a b b b π 1 = π 2 = 1 / 2 \pi_1 = \pi_2 = 1/2 π 1 = π 2 = 1/2

The long-run payoffs of two reactive strategies in the Prisoner’s Dilemma

(see Direct Reciprocity 4 × 4 4 \times 4 4 × 4 { C C , C D , D C , D D } \{CC, CD, DC, DD\} { CC , C D , D C , DD }

Consider the special case of two tit-for-tat players: ( p , q ) = ( 1 , 0 ) (p, q) = (1, 0) ( p , q ) = ( 1 , 0 ) ( p ′ , q ′ ) = ( 1 , 0 ) (p', q') = (1, 0) ( p ′ , q ′ ) = ( 1 , 0 )

Write down the 4 × 4 4 \times 4 4 × 4

Is this chain ergodic? Explain why or why not.

If the game starts in state C C CC CC

Programming ¶ Computing the Stationary Distribution with NumPy ¶ The stationary distribution π \pi π π P = π \pi P = \pi π P = π π ( P − I ) = 0 \pi (P - I) = 0 π ( P − I ) = 0 ∑ i π i = 1 \sum_i \pi_i = 1 ∑ i π i = 1

import numpy as np

def stationary_distribution(P):

"""Compute the stationary distribution of an ergodic transition matrix."""

n = P.shape[0]

A = (P - np.eye(n)).T

# Replace last row with normalisation constraint

A[-1, :] = 1.0

b = np.zeros(n)

b[-1] = 1.0

return np.linalg.solve(A, b)

# Weather example

P_weather = np.array([[0.7, 0.3],

[0.6, 0.4]])

pi = stationary_distribution(P_weather)

print(f"Stationary distribution: Sunny={pi[0]:.4f}, Rainy={pi[1]:.4f}")Stationary distribution: Sunny=0.6667, Rainy=0.3333

Verifying Convergence ¶ We can verify the Ergodic Theorem numerically by powering the transition matrix:

# Confirm convergence: P^t rows all approach pi as t grows large

P_power = np.linalg.matrix_power(P_weather, 50)

print("P^50 (rows should all equal stationary distribution):")

print(np.round(P_power, 6))P^50 (rows should all equal stationary distribution):

[[0.666667 0.333333]

[0.666667 0.333333]]

Stationary Distribution of a 3-State Chain ¶ P_3 = np.array([[0.0, 0.6, 0.4],

[0.3, 0.0, 0.7],

[0.5, 0.5, 0.0]])

pi_3 = stationary_distribution(P_3)

print(f"Stationary distribution: {np.round(pi_3, 4)}")

# Verify: pi @ P should equal pi

print(f"Verification pi @ P: {np.round(pi_3 @ P_3, 4)}")Stationary distribution: [0.2863 0.3524 0.3612]

Verification pi @ P: [0.2863 0.3524 0.3612]

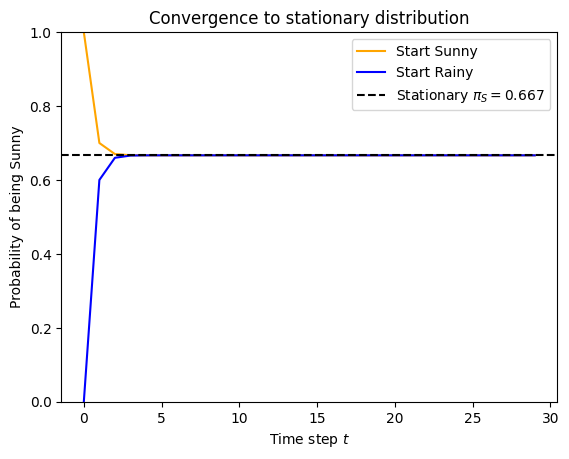

Visualising Convergence from Different Starting States ¶ import matplotlib.pyplot as plt

T = 30

pi_0_sunny = np.array([1.0, 0.0]) # start Sunny

pi_0_rainy = np.array([0.0, 1.0]) # start Rainy

dist_sunny = [pi_0_sunny @ np.linalg.matrix_power(P_weather, t) for t in range(T)]

dist_rainy = [pi_0_rainy @ np.linalg.matrix_power(P_weather, t) for t in range(T)]

plt.figure()

plt.plot([d[0] for d in dist_sunny], label="Start Sunny", color="orange")

plt.plot([d[0] for d in dist_rainy], label="Start Rainy", color="blue")

plt.axhline(pi[0], color="black", linestyle="--", label=f"Stationary $\\pi_S={pi[0]:.3f}$")

plt.xlabel("Time step $t$")

plt.ylabel("Probability of being Sunny")

plt.title("Convergence to stationary distribution")

plt.legend()

plt.ylim(0, 1);Notable Research ¶ The theory of ergodic Markov chains builds on the foundational work of Andrei

Markov himself, who first studied the long-run behaviour of dependent random

sequences in the early twentieth century.

The modern treatment of ergodic chains and stationary distributions is

presented in the classical reference Kemeny & Snell, 1976

The application of ergodic theory to repeated games and direct reciprocity

is central to the analysis of reactive strategies in the Prisoner’s Dilemma,

as explored in Direct Reciprocity Press & Dyson, 2012

Conclusion ¶ This appendix introduced ergodic Markov chains and the Ergodic Theorem ,

which guarantees convergence to a unique stationary distribution for chains

that are irreducible and aperiodic. These tools are essential for analysing

systems that cycle indefinitely rather than being absorbed.

The key concepts are summarised in Table A3.1

Table A3.1: Summary of ergodic Markov chains

Concept Description Irreducible Chain Every state is reachable from every other state Aperiodic Chain No state is locked into returning only at multiples of a fixed period Ergodic Chain Irreducible and aperiodic; converges to a unique stationary distribution Stationary Distribution π P = π \pi P = \pi π P = π ∑ π i = 1 \sum \pi_i = 1 ∑ π i = 1 Ergodic Theorem π ( 0 ) P t → π \pi^{(0)} P^t \to \pi π ( 0 ) P t → π π ( 0 ) \pi^{(0)} π ( 0 )

The stationary distribution of an ergodic Markov chain provides the long-run

time average of any observable quantity. This makes it the key tool for

computing long-run payoffs in repeated games and evolutionary models with

ongoing interaction, as opposed to absorbing chains where the relevant

quantity is the probability of reaching each terminal state.

Solutions ¶ 1. P = ( 0 1 1 0 ) P = \begin{pmatrix}0 & 1 \\ 1 & 0\end{pmatrix} P = ( 0 1 1 0 )

Irreducible? Yes: from state 1 we reach state 2 in one step, and from

state 2 we reach state 1 in one step.

Aperiodic? No. The period of each state is d = 2 d = 2 d = 2 P P P P 2 = I P^2 = I P 2 = I

Ergodic? No (not aperiodic).

Since the chain is not ergodic, the Ergodic Theorem does not apply in its

strong form. However, because the chain is irreducible, there is still a

unique stationary distribution. Solving π P = π \pi P = \pi π P = π π 1 + π 2 = 1 \pi_1 + \pi_2 = 1 π 1 + π 2 = 1 π 2 = π 1 \pi_2 = \pi_1 π 2 = π 1 π = ( 1 / 2 , 1 / 2 ) \pi = (1/2, 1/2) π = ( 1/2 , 1/2 ) ( 1 / 2 , 1 / 2 ) (1/2, 1/2) ( 1/2 , 1/2 )

2. P = ( 0.5 0.5 0.3 0.7 ) P = \begin{pmatrix}0.5 & 0.5 \\ 0.3 & 0.7\end{pmatrix} P = ( 0.5 0.3 0.5 0.7 )

Irreducible? Yes: both off-diagonal entries are positive.

Aperiodic? Yes: both diagonal entries are positive (P 11 = 0.5 > 0 P_{11} = 0.5 > 0 P 11 = 0.5 > 0 P 22 = 0.7 > 0 P_{22} = 0.7 > 0 P 22 = 0.7 > 0 d i = 1 d_i = 1 d i = 1

Ergodic? Yes.

Stationary distribution. Solving π P = π \pi P = \pi π P = π

0.5 π 1 + 0.3 π 2 = π 1 ⟹ 0.3 π 2 = 0.5 π 1 ⟹ π 1 = 3 5 π 2 0.5 \pi_1 + 0.3 \pi_2 = \pi_1 \implies 0.3 \pi_2 = 0.5 \pi_1 \implies \pi_1 = \frac{3}{5}\pi_2 0.5 π 1 + 0.3 π 2 = π 1 ⟹ 0.3 π 2 = 0.5 π 1 ⟹ π 1 = 5 3 π 2 With π 1 + π 2 = 1 \pi_1 + \pi_2 = 1 π 1 + π 2 = 1

3 5 π 2 + π 2 = 1 ⟹ π 2 = 5 8 , π 1 = 3 8 . \frac{3}{5}\pi_2 + \pi_2 = 1 \implies \pi_2 = \frac{5}{8}, \quad \pi_1 = \frac{3}{8}. 5 3 π 2 + π 2 = 1 ⟹ π 2 = 8 5 , π 1 = 8 3 . So π = ( 3 / 8 , 5 / 8 ) = ( 0.375 , 0.625 ) \pi = (3/8,\ 5/8) = (0.375,\ 0.625) π = ( 3/8 , 5/8 ) = ( 0.375 , 0.625 )

3. P = ( 1 0 0 0 0.5 0.5 0 0.5 0.5 ) P = \begin{pmatrix}1 & 0 & 0 \\ 0 & 0.5 & 0.5 \\ 0 & 0.5 & 0.5\end{pmatrix} P = ⎝ ⎛ 1 0 0 0 0.5 0.5 0 0.5 0.5 ⎠ ⎞

Irreducible? No. State 1 has P 11 = 1 P_{11} = 1 P 11 = 1

Aperiodic? State 1 is aperiodic (self-loop). States 2 and 3 have

period 1 since P 2 P^2 P 2

Ergodic? No (not irreducible).

The chain has multiple closed communicating classes and is therefore not

ergodic; there is no unique stationary distribution for any initial state.

import numpy as np

def stationary_distribution(P):

n = P.shape[0]

A = (P - np.eye(n)).T

A[-1, :] = 1.0

b = np.zeros(n)

b[-1] = 1.0

return np.linalg.solve(A, b)

P2 = np.array([[0.5, 0.5], [0.3, 0.7]])

pi2 = stationary_distribution(P2)

print("Chain 2 stationary distribution:", np.round(pi2, 6))

# Verify

print("Verification pi @ P:", np.round(pi2 @ P2, 6))Chain 2 stationary distribution: [0.375 0.625]

Verification pi @ P: [0.375 0.625]

Let P = ( 1 − a a b 1 − b ) P = \begin{pmatrix}1-a & a \\ b & 1-b\end{pmatrix} P = ( 1 − a b a 1 − b ) 0 < a , b < 1 0 < a, b < 1 0 < a , b < 1

Ergodicity. Since a > 0 a > 0 a > 0 b > 0 b > 0 b > 0 irreducible . The diagonal entries satisfy 1 − a ∈ ( 0 , 1 ) 1 - a \in (0, 1) 1 − a ∈ ( 0 , 1 ) 1 − b ∈ ( 0 , 1 ) 1 - b \in (0, 1) 1 − b ∈ ( 0 , 1 ) d i = 1 d_i = 1 d i = 1 i i i aperiodic . Hence it is ergodic for any

a , b ∈ ( 0 , 1 ) a, b \in (0, 1) a , b ∈ ( 0 , 1 )

Stationary distribution. The condition π P = π \pi P = \pi π P = π

π 1 ( 1 − a ) + π 2 b = π 1 ⟹ π 1 a = π 2 b ⟹ π 1 = b a π 2 . \pi_1(1 - a) + \pi_2 b = \pi_1 \implies \pi_1 a = \pi_2 b \implies \pi_1 = \frac{b}{a}\pi_2. π 1 ( 1 − a ) + π 2 b = π 1 ⟹ π 1 a = π 2 b ⟹ π 1 = a b π 2 . Using π 1 + π 2 = 1 \pi_1 + \pi_2 = 1 π 1 + π 2 = 1

b a π 2 + π 2 = 1 ⟹ π 2 a + b a = 1 ⟹ π 2 = a a + b . \frac{b}{a}\pi_2 + \pi_2 = 1 \implies \pi_2\frac{a + b}{a} = 1 \implies \pi_2 = \frac{a}{a + b}. a b π 2 + π 2 = 1 ⟹ π 2 a a + b = 1 ⟹ π 2 = a + b a . Therefore:

π 1 = b a + b , π 2 = a a + b . \pi_1 = \frac{b}{a + b}, \qquad \pi_2 = \frac{a}{a + b}. π 1 = a + b b , π 2 = a + b a . Condition for uniform stationary distribution. We need π 1 = π 2 = 1 / 2 \pi_1 = \pi_2 = 1/2 π 1 = π 2 = 1/2

b a + b = 1 2 ⇔ 2 b = a + b ⇔ a = b . \frac{b}{a + b} = \frac{1}{2} \Leftrightarrow 2b = a + b \Leftrightarrow a = b. a + b b = 2 1 ⇔ 2 b = a + b ⇔ a = b . The stationary distribution is uniform if and only if a = b a = b a = b

import sympy as sym

a, b = sym.symbols("a b", positive=True)

P_sym = sym.Matrix([[1 - a, a], [b, 1 - b]])

pi1, pi2 = sym.symbols("pi_1 pi_2")

eqs = [

sym.Eq(pi1 * (1 - a) + pi2 * b, pi1),

sym.Eq(pi1 + pi2, 1),

]

sol = sym.solve(eqs, [pi1, pi2])

print("Stationary distribution:")

print("pi_1 =", sol[pi1])

print("pi_2 =", sol[pi2])Stationary distribution:

pi_1 = b/(a + b)

pi_2 = a/(a + b)

# Condition for pi_1 = pi_2

condition = sym.solve(sym.Eq(sol[pi1], sym.Rational(1, 2)), a)

print("Condition for uniform distribution: a =", condition)Condition for uniform distribution: a = [b]

The weather chain from Motivating Example: Long-Run Behaviour in a Cycling System

P = ( 0.7 0.3 0.6 0.4 ) P = \begin{pmatrix}0.7 & 0.3 \\ 0.6 & 0.4\end{pmatrix} P = ( 0.7 0.6 0.3 0.4 ) with α = 0.3 \alpha = 0.3 α = 0.3 β = 0.6 \beta = 0.6 β = 0.6 π = ( 2 / 3 , 1 / 3 ) \pi = (2/3, 1/3) π = ( 2/3 , 1/3 )

Computing π ( 1 ) \pi^{(1)} π ( 1 ) π ( 2 ) \pi^{(2)} π ( 2 ) π ( 0 ) = ( 1 , 0 ) \pi^{(0)} = (1, 0) π ( 0 ) = ( 1 , 0 )

π ( 1 ) = π ( 0 ) P = ( 1 , 0 ) ( 0.7 0.3 0.6 0.4 ) = ( 0.7 , 0.3 ) . \begin{align*}

\pi^{(1)} &= \pi^{(0)} P = (1, 0) \begin{pmatrix}0.7 & 0.3 \\ 0.6 & 0.4\end{pmatrix} \\

&= (0.7,\ 0.3).

\end{align*} π ( 1 ) = π ( 0 ) P = ( 1 , 0 ) ( 0.7 0.6 0.3 0.4 ) = ( 0.7 , 0.3 ) . π ( 2 ) = π ( 1 ) P = ( 0.7 , 0.3 ) ( 0.7 0.3 0.6 0.4 ) = ( 0.7 × 0.7 + 0.3 × 0.6 , 0.7 × 0.3 + 0.3 × 0.4 ) = ( 0.49 + 0.18 , 0.21 + 0.12 ) = ( 0.67 , 0.33 ) . \begin{align*}

\pi^{(2)} &= \pi^{(1)} P = (0.7, 0.3) \begin{pmatrix}0.7 & 0.3 \\ 0.6 & 0.4\end{pmatrix} \\

&= (0.7 \times 0.7 + 0.3 \times 0.6,\ 0.7 \times 0.3 + 0.3 \times 0.4) \\

&= (0.49 + 0.18,\ 0.21 + 0.12) \\

&= (0.67,\ 0.33).

\end{align*} π ( 2 ) = π ( 1 ) P = ( 0.7 , 0.3 ) ( 0.7 0.6 0.3 0.4 ) = ( 0.7 × 0.7 + 0.3 × 0.6 , 0.7 × 0.3 + 0.3 × 0.4 ) = ( 0.49 + 0.18 , 0.21 + 0.12 ) = ( 0.67 , 0.33 ) . Distance from the stationary distribution. The stationary distribution

is π = ( 2 / 3 , 1 / 3 ) ≈ ( 0.6 6 ‾ , 0.3 3 ‾ ) \pi = (2/3, 1/3) \approx (0.6\overline{6}, 0.3\overline{3}) π = ( 2/3 , 1/3 ) ≈ ( 0.6 6 , 0.3 3 )

∥ π ( 2 ) − π ∥ 1 = ∣ 0.67 − 0.6 6 ‾ ∣ + ∣ 0.33 − 0.3 3 ‾ ∣ = 0.003 3 ‾ + 0.003 3 ‾ ≈ 0.0067. \begin{align*}

\|\pi^{(2)} - \pi\|_1 &= |0.67 - 0.6\overline{6}| + |0.33 - 0.3\overline{3}| \\

&= 0.003\overline{3} + 0.003\overline{3} \approx 0.0067.

\end{align*} ∥ π ( 2 ) − π ∥ 1 = ∣0.67 − 0.6 6 ∣ + ∣0.33 − 0.3 3 ∣ = 0.003 3 + 0.003 3 ≈ 0.0067. After only two steps, the distribution is within less than 1% of the

stationary distribution in ℓ 1 \ell^1 ℓ 1

Eigenvalues of P P P The characteristic polynomial of P P P

det ( P − λ I ) = ( 0.7 − λ ) ( 0.4 − λ ) − ( 0.3 ) ( 0.6 ) = λ 2 − 1.1 λ + ( 0.28 − 0.18 ) = λ 2 − 1.1 λ + 0.10. \begin{align*}

\det(P - \lambda I) &= (0.7 - \lambda)(0.4 - \lambda) - (0.3)(0.6) \\

&= \lambda^2 - 1.1\lambda + (0.28 - 0.18) \\

&= \lambda^2 - 1.1\lambda + 0.10.

\end{align*} det ( P − λ I ) = ( 0.7 − λ ) ( 0.4 − λ ) − ( 0.3 ) ( 0.6 ) = λ 2 − 1.1 λ + ( 0.28 − 0.18 ) = λ 2 − 1.1 λ + 0.10. The roots are:

λ = 1.1 ± 1.21 − 0.4 2 = 1.1 ± 0.81 2 = 1.1 ± 0.9 2 . \begin{align*}

\lambda &= \frac{1.1 \pm \sqrt{1.21 - 0.4}}{2} = \frac{1.1 \pm \sqrt{0.81}}{2} \\

&= \frac{1.1 \pm 0.9}{2}.

\end{align*} λ = 2 1.1 ± 1.21 − 0.4 = 2 1.1 ± 0.81 = 2 1.1 ± 0.9 . So λ 1 = 1 \lambda_1 = 1 λ 1 = 1 λ 2 = 0.1 \lambda_2 = 0.1 λ 2 = 0.1

Verification: ∣ 1 − α − β ∣ = ∣ 1 − 0.3 − 0.6 ∣ = ∣ 0.1 ∣ = 0.1 = ∣ λ 2 ∣ |1 - \alpha - \beta| = |1 - 0.3 - 0.6| = |0.1| = 0.1 = |\lambda_2| ∣1 − α − β ∣ = ∣1 − 0.3 − 0.6∣ = ∣0.1∣ = 0.1 = ∣ λ 2 ∣

The second eigenvalue governs the exponential rate of convergence:

∣ λ 2 ∣ t = 0. 1 t |\lambda_2|^t = 0.1^t ∣ λ 2 ∣ t = 0. 1 t ∣ λ 2 ∣ 2 = 0.01 |\lambda_2|^2 = 0.01 ∣ λ 2 ∣ 2 = 0.01

import numpy as np

P = np.array([[0.7, 0.3], [0.6, 0.4]])

pi_0 = np.array([1.0, 0.0])

pi_1 = pi_0 @ P

pi_2 = pi_1 @ P

print("pi^(1) =", pi_1)

print("pi^(2) =", pi_2)

pi_stationary = np.array([2/3, 1/3])

print("Stationary distribution:", np.round(pi_stationary, 6))

print("L1 distance after 2 steps:", np.sum(np.abs(pi_2 - pi_stationary)))pi^(1) = [0.7 0.3]

pi^(2) = [0.67 0.33]

Stationary distribution: [0.666667 0.333333]

L1 distance after 2 steps: 0.006666666666666654

eigenvalues = np.linalg.eigvals(P)

print("Eigenvalues of P:", np.sort(eigenvalues)[::-1])

alpha, beta = 0.3, 0.6

print("|1 - alpha - beta| =", abs(1 - alpha - beta))Eigenvalues of P: [1. 0.1]

|1 - alpha - beta| = 0.09999999999999998

Two tit-for-tat (TFT) players with ( p , q ) = ( 1 , 0 ) (p, q) = (1, 0) ( p , q ) = ( 1 , 0 ) { C C , C D , D C , D D } \{CC, CD, DC, DD\} { CC , C D , D C , DD }

Transition matrix. Given current state (row player’s last action,

column player’s last action):

From C C CC CC C C C C C C p = 1 p=1 p = 1 C C C C C C p ′ = 1 p'=1 p ′ = 1 C C CC CC

From C D CD C D D D D D D D q = 0 q=0 q = 0 C C C C C C p ′ = 1 p'=1 p ′ = 1 D C DC D C

From D C DC D C C C C C C C p = 1 p=1 p = 1 D D D D D D q ′ = 0 q'=0 q ′ = 0 C D CD C D

From D D DD DD D D D D D D q = 0 q=0 q = 0 D D D D D D q ′ = 0 q'=0 q ′ = 0 D D DD DD

The transition matrix (ordering states C C , C D , D C , D D CC, CD, DC, DD CC , C D , D C , DD

P = ( 1 0 0 0 0 0 1 0 0 1 0 0 0 0 0 1 ) P = \begin{pmatrix}

1 & 0 & 0 & 0 \\

0 & 0 & 1 & 0 \\

0 & 1 & 0 & 0 \\

0 & 0 & 0 & 1

\end{pmatrix} P = ⎝ ⎛ 1 0 0 0 0 0 1 0 0 1 0 0 0 0 0 1 ⎠ ⎞ Ergodicity. The chain is not ergodic :

State C C CC CC P C C , C C = 1 P_{CC,CC} = 1 P CC , CC = 1

State D D DD DD P D D , D D = 1 P_{DD,DD} = 1 P DD , DD = 1

States C D CD C D D C DC D C C D → D C → C D → ⋯ CD \to DC \to CD \to \cdots C D → D C → C D → ⋯

The chain is reducible : state C C CC CC D D DD DD { C D , D C } \{CD,DC\} { C D , D C }

Therefore the chain is neither irreducible nor aperiodic, hence not ergodic.

Long-run distribution starting from C C CC CC Since C C CC CC C C CC CC C C CC CC

π = ( 1 , 0 , 0 , 0 ) (all probability in state C C ) . \pi = (1, 0, 0, 0) \quad \text{(all probability in state } CC\text{)}. π = ( 1 , 0 , 0 , 0 ) (all probability in state CC ) . In terms of the game: two TFT players who start by cooperating will

cooperate forever. The long-run payoff per round equals the cooperation

payoff R R R

import numpy as np

# TFT vs TFT transition matrix over states {CC, CD, DC, DD}

P_tft = np.array([

[1, 0, 0, 0], # CC -> CC

[0, 0, 1, 0], # CD -> DC

[0, 1, 0, 0], # DC -> CD

[0, 0, 0, 1], # DD -> DD

], dtype=float)

print("Transition matrix P:")

print(P_tft)

# Starting from CC (index 0), pi^(0) = (1, 0, 0, 0)

pi_0 = np.array([1.0, 0.0, 0.0, 0.0])

print("\nAfter 10 steps (from CC):", pi_0 @ np.linalg.matrix_power(P_tft, 10))Transition matrix P:

[[1. 0. 0. 0.]

[0. 0. 1. 0.]

[0. 1. 0. 0.]

[0. 0. 0. 1.]]

After 10 steps (from CC): [1. 0. 0. 0.]

Kemeny, J. G., & Snell, J. L. (1976). Finite Markov chains . Springer-Verlag. Press, W. H., & Dyson, F. J. (2012). Iterated Prisoner’s Dilemma contains strategies that dominate any evolutionary opponent. Proceedings of the National Academy of Sciences , 109 (26), 10409–10413.