Sold: A Python library for the study of Acutions

I have been playing around with auction theory, I put sold together which lets you simulate auctions:

https://github.com/drvinceknight/sold

Here is some code to simulate a second pay auction where 1 of the bidders shades their bid (optimal behaviour in a first pay auction) and the other bids their true value.

import scipy.stats

import numpy as np

import matplotlib.pyplot as plt

import sold.allocate

import sold.bid

import sold.pay

N = 2

repetitions = 50_000

shade_steps = 9

shades = np.linspace(0, 1, shade_steps)

valuation_distributions = [scipy.stats.uniform for _ in range(N)]

utility = np.zeros(shape=(N, repetitions, shade_steps))

for i, shade in enumerate(shades):

bidding_functions = [sold.bid.create_shaded_bid_map(shade), sold.bid.true_value]

for seed in range(repetitions):

allocation, payments, valuations = sold.auction(

valuation_distributions=valuation_distributions,

bidding_functions=bidding_functions,

allocation_rule=sold.allocate.first_price,

payment_rule=sold.pay.second_price,

seed=seed,

)

utility[:, seed, i] = allocation * valuations - payments

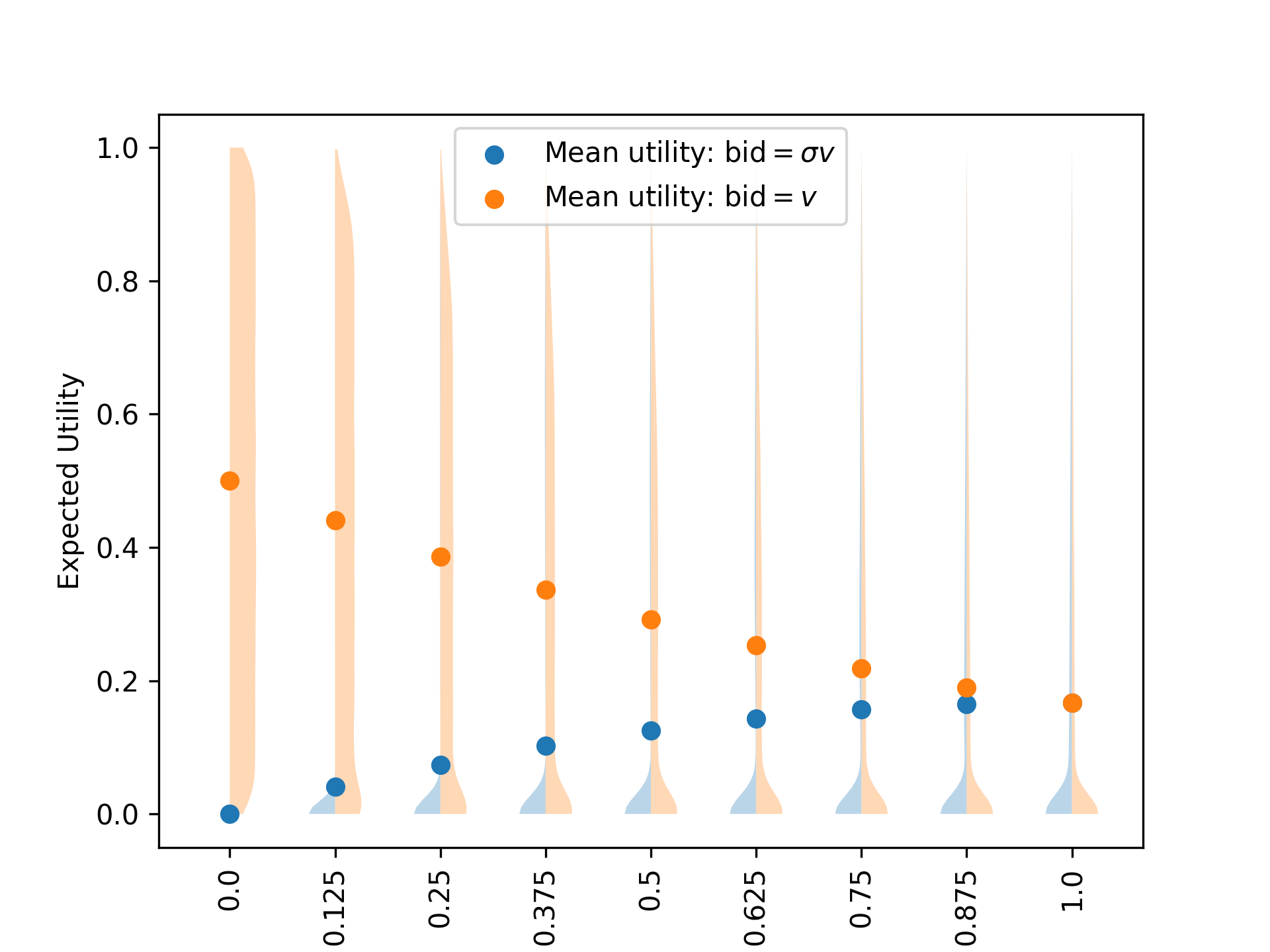

The true value is known to be weakly dominant in a second pay auction) which is kind of what is confirmed by this plot:

plt.figure()

plt.violinplot(

utility[0],

showmeans=False,

showmedians=False,

showextrema=False,

side="low",

)

plt.violinplot(

utility[1],

showmeans=False,

showmedians=False,

showextrema=False,

side="high",

)

plt.scatter(range(1, shade_steps + 1), np.mean(utility[0], axis=0), label=r"Mean utility: bid$=\sigma v$")

plt.scatter(range(1, shade_steps + 1), np.mean(utility[1], axis=0), label=r"Mean utility: bid$=v$")

plt.xlabel(r"Shade value $\sigma$")

plt.xticks(range(1, shade_steps + 1), shades, rotation=90)

plt.ylabel("Expected Utility")

plt.legend()

plt.show()

If anyone wants to play around with it you can python -m pip install sold or even better you can look through the code base

(I have no idea if this is something I plan to return to or just leave it as is).